Allocation Funds

In late 2025, the Plan transitioned the conservative through aggressive allocation models into conservative through aggressive allocation funds. Whether using a model or a single fund, the goal of these investments is to provide a diversified approach to a given risk-return parameter.

Why use a diversified portfolio?

A diversified portfolio spreads your investments across different asset classes, sectors, and geographic regions to reduce risk—if one investment performs poorly, others may offset those losses. This approach helps smooth out returns over time and protects you from the catastrophic impact of putting all your eggs in one basket, while still allowing you to participate in market growth.

Why we fell allocation funds work well in this Plan.

This plan is unique compared to a conventional 401(k) retirement plan. The reason is that the bulk of your future retirement income will come from the pension plan. The deferred compensation plan is a voluntary benefit, and participants use it for multiple reasons, not just retirement income. In fact, after many years of servicing this plan, I found that most people do not use it for retirement income. Because of this, I think allocation funds can be a better fit than target date funds for most participants. Target date funds can work out great when you are younger, but as you approach retirement, they might not be the most suitable because a target date fund is designed to provide lifetime income. If you plan on liquidating the deferred compensation account soon after retirement, a target date fund might be more aggressively invested than is ideal for that situation. Therefore, I feel that selecting the right allocation fund and adjusting it to become more conservative as you move toward retirement can be a better approach than target date funds if you are not seeking to provide lifetime income from this account.

Which fund is right for me?

We have made it easy to select the correct allocation fund. Just follow the steps below:

Step 1: Take Risk Profile

Answer the questions in the Risk Profile.

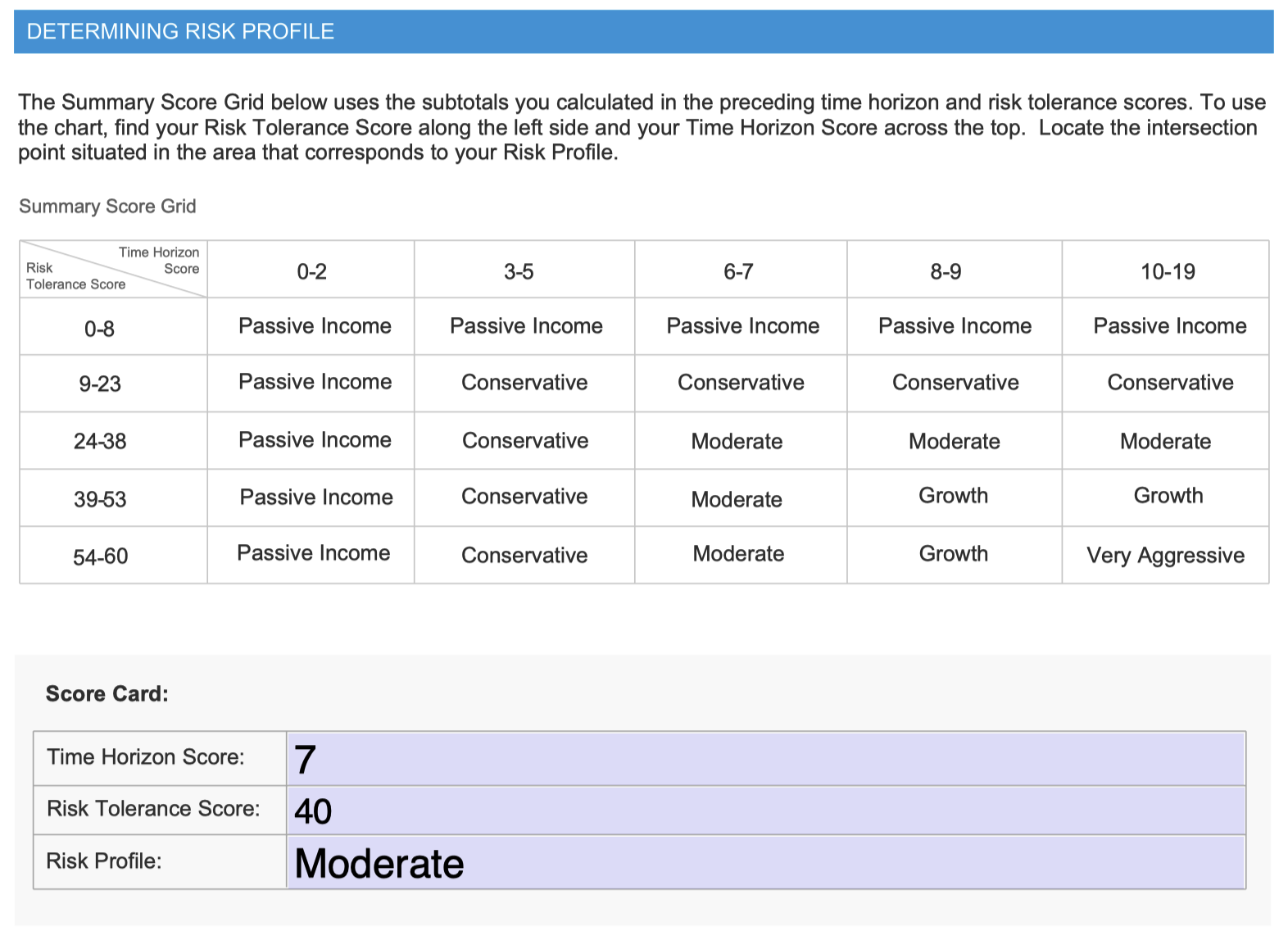

The risk profile is broken down into two sections. The first is your time horizon, and the second is your risk tolerance. These sections are scored independently. The reason why is that if you have a longer time horizon—the period of time until your account is liquidated—then you have more time to weather the ups and downs in the markets. For example, if you are a very cautious person who is afraid of losing money, it would not be ideal to have all your money in a money market fund for decades. Likewise, if you are a very aggressive investor but you need to liquidate the account in the next few months, it would not be ideal to have all your money in the stock market. The risk tolerance portion is also important because you do not want to be too aggressively invested so that when you do lose money, you do not sell everything and move to something more conservative towards a market bottom. If you do this, it may take you a very long time to make up those losses. It would be better to be more conservative from the onset and stay consistent with the investment.

Step 2: Score Risk Profile

Add up your Time Horizon Score and Risk Tolerance Score to determine you overall Profile Score.

In this example, with a time horizon score of 7 and a risk tolerance score of 40, the overall risk profile would be moderate.

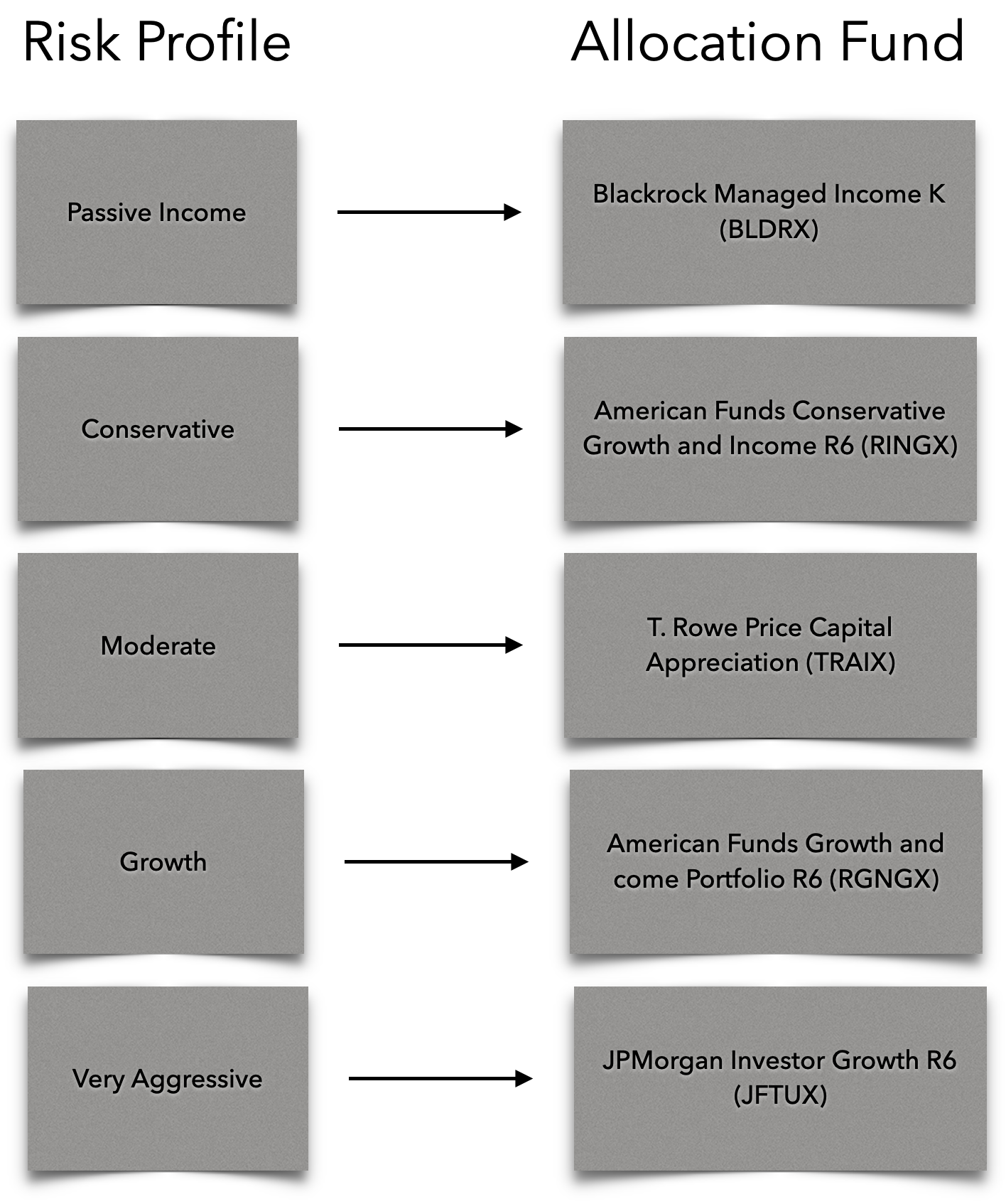

Step 3: Select allocation fund

Once you have determined your risk profile, use the chart below to select the appropriate allocation fund.

We recommend selecting only one allocation fund. If you would like to diversify your approach to investing, you could consider pairing an allocation fund with a target date fund or tactical model, but typically an investor would only select one allocation fund.